MedPlus IPO — Here’s All You Need to Know

MedPlus Health Services Ltd. (hereinafter referred to as “MedPlus”), India’s second-largest pharmacy retailer, obtained SEBI’s assent to launch an IPO in December.

We bring you the exclusive low-down on the company before you decide to invest.

IPO Stats

- Issue Size: ₹1,638.71cr ($218.4m) (Fresh Issue: ₹600cr ($80m) + Offer for Sale: ₹1,038.71cr ($137.3))

- Selling Shareholders: PI Opportunities (₹500cr ($66.6m)) + Lone Furrow Investments (₹450cr ($60m)) + smaller shareholders, including promoters (₹89cr ($11.8m))

- Face Value of Equity Shares: ₹2

The startup is backed by Warburg Pincus and the IPO could potentially raise its valuation to north of $1bn or a 25x+ EV/Adj EBITDA. Post-listing, MedPlus would become the country’s first listed retail pharmacy chain.

The fresh issue component of the IPO is aimed to be used towards working capital purposes. The company will also use part of the funds raised to finance its subsidiary, Optival Health Solutions.

Company Profile and Business

MedPlus is a Hyderabad-based pharmacy retailer that was founded in 2006 by Gangadi Madhukar Reddy who is its Managing Director and CEO. Some of its early investors included India Venture Advisors (owned by Ajay Piramal), Mount Kellett Capital Management and TVS Capital Funds. All of the above were bought out by MedPlus in January 2018 after it raised $115m in debt funding from Goldman Sachs.

It offers a wide range of products largely in the pharmaceutical and wellness category such as medicines, vitamins, medical devices, test kits, FMCG products, home and personal care products including toiletries, soaps, detergents, sanitizers, baby care products etc. It also reportedly runs a diagnostics service and optical lens store and B2B medical supplies business.

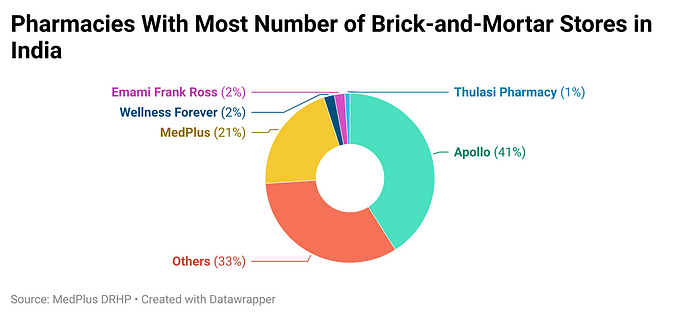

Initially operating out of 48 stores, the company has now grown to 2,000 retail units in the country, trailing slightly behind Apollo. It tops the store numbers in the states of Karnataka, Tamil Nadu and Telangana.

The company offers both offline and online (through MedPlus Mart) sales of pharmaceuticals. Expanding its online presence and to other states (beyond the seven it currently maintains a presence in) remains crucial to the company so as to compete alongside PharmEasy, another startup which is currently India’s largest online pharmacy retailer.

Company Financials

The company operates in a business that is heavily working capital-intensive. A large portion of the working capital is also used towards inventories. As it grows, so will the working capital needs. But having substantial indebtedness, especially through Optival, has resulted in negative cash flows in the last three financial years.

Between FY19 and FY21, revenue from operations grew at a CAGR of 16.21% as opposed to the Indian pharmacy retail industry as a whole which grew at 7.3% during the same period. Adjusted EBITDA also increased by 43.98% during that period showing strong financial performance (pg. 121, DRHP).

The cluster-based expansion and replicable roll-out strategy has assisted in the company maintaining healthy store-level economics (Average Revenue per Store (annually) = ₹15.9m ($212,057), which is more than the industry average). MedPlus was also the first pharmacy retailer in India to offer an omni-channel platform (both store-based and online offerings).

A promising indication of growth lies in the fact that the company’s online sales have accounted for 8.98% and 6.99% of its total operating revenue in FY20 and FY21 respectively, showing steady increase (pg. 120, DRHP).

With brand presence of over 15 years in the Indian markets, advantage seems to favour MedPlus when it comes to expansion plans. Continued cost-cutting measures in the form of retail discounts offered by the company are a massive bonus. In terms of delivery capabilities, the company has also acquired a positive reputation, ensuring within-two-hour deliveries in select cities, a practice it aims to further in other locations as well.

Industry Overview

India’s e-commerce pharmacy retail market is expected to grow at a CAGR of c. 42% between FY21 and FY25.

Agreed, the per-capita healthcare expenditure in India is one of the lowest in the world. But given the broader optics of growth in the domestic pharma sector (propelled in part by the pandemic’s effect because of pharmacy being an “essential service”), the industry has risen at a healthy 10% CAGR in the last five years offering enough room for companies to reign in and channel the growth momentum (pg 104, DRHP).

Having said that, the industry in question is highly competitive. The global pharmaceutical supply chain is not only complex but also quite varied. Pharmacy retail companies form a part of this gigantic chain catering to the end-user segment which includes over-the-counter prescription drugs and related products.

When it comes to brick-and-mortar stores, leading players like Apollo and Emami lead the industry with their vast, traditional and pan-India presence in the organised segment. But there has also been a commensurate rise in pharma sales through the e-commerce channel over the past decade with emerging players like PharmEasy, NetMeds, Tata 1mg and MedPlus.

The latter category of players largely functions on a hyperlocal model which is backed by robust logistics. Being an established player, therefore, plays to a huge advantage due to better brand visibility and low customer acquisition costs which plays well with unit economics, especially when working capital needs are escalating owing to the expansion demands.

MedPlus, which has a pocketed presence in seven states, is better equipped than many others to capitalise on this demand and grow through its existing multichannel operation.

Reading the IPO Room

The online pharmacy industry may be on the rise but it is still at a nascent stage of development. MedPlus has to compete with rivals who have longer operating histories, larger customer bases, greater brand recognition and more extensive commercial relationships (in certain markets).

But with promising unit economics, macro indicators (timely deliveries, cost discounts, etc.) and a robust product portfolio across some major states, the company looks poised to plod down the growth lane in future.

Product supply chains, however, could be a variable that can hamper growth dynamics in the long run seeing as MedPlus relies on third-party manufacturers for the supply of products. The cash and credit facilities availed by Optival from various lenders should also be factored in when looked at the company’s financials.

That being said, with a sound-performing backward-integrated value chain and wholly-managed operations through technology-driven supply and distribution networks, MedPlus certainly gains leverage to further its business in the long run. This is also cemented by the fact that the company boasts of a marquee history in terms of investors like Lavender Rose (part of Warburg Pincus group) and affiliates of PremjiInvest (Azim Premji-led) which could boost investor confidence to a great extent.

Looking forward to yet another market debut with bated breath! ;)

(Originally published December 3rd 2021 in transfin.in)