All About the OYO IPO

India’s third-most valuable startup is now headed for an IPO. Oravel Stays Pvt. Ltd., the parent company of the hospitality unicorn OYO Hotels and Homes, has filed the prospectus for an IPO valued at $1.1bn. (Link to DRHP.).

With this, OYO joins a school of startups including Paytm, Nykaa, ixigo and Policybazaar who have filed for an IPO this year. It will also become the fourth Indian travel and hospitality startup heading towards a public listing (after EaseMyTrip, ixigo and RateGain).

Besides indicating a remarkable recovery in the Indian markets post-pandemic, this IPO is also a sign of the company fashioning a comeback in a business which had been lately saddled with financial stress, embittered relationships with hotel owners and litigation.

We bring you here an exclusive, detailing the finer points of this IPO.

Fast Facts

- Issue Size: ₹8,430cr ($1.1bn) divided into ₹7,000cr ($946.7m) in fresh issue and ₹1,430cr ($193.4m) in an offer for sale (OFS).

- Price Band: Undeclared as of now.

- Issue Type: Book Building.

- Issue Breakup: QIBs — 75%, NIIs — 15% and retail investors — 10%.

- The company may consider issuing shares up to ₹1,400cr ($189.3m) in a pre-IPO placement.

- A part of the net proceeds are proposed to be used for: (a) prepayment/repayment of debts worth ₹2,441cr ($330.1m), (b) funding organic and inorganic growth initiatives worth ₹2,900cr ($392.2m).

The IPO is going to be a mix of both primary and secondary sales and is planning to list by the end of the year. The founder Ritesh Agarwal along with his company RA Hospitality Holdings will be retaining their 33.16% stake in OYO whereas other major investors like SoftBank (SVF India Holdings), Grab (A1 Holdings), HuaZhu Hotels (China Lodging Holdings), Global Ivy Ventures etc. Are planning to offload a part of their stakes.

Company Profile

OYO was launched in 2013 by Ritesh Agarwal with the aim of creating a budget hotel aggregator business in India. The Gurugram-based company reportedly operates through 159 trademark registrations in India including OYO Hotels, OYO Inns, OYO Rooms, OYO Townhouse, OYO WokeSoap, OYO Homes, Silverkey etc.

As per the prospectus, the app has been downloaded over 100 million times placing it alongside other popular travel apps like Airbnb and Booking.com. The company has a number of marquee investors — SoftBank, Airbnb, Lightspeed Venture Partners, Sequoia Capital, Innoven etc and most recently, Microsoft. It has raised $4.1bn from 26 investors in 19 funding rounds so far.

Currently, OYO has more than 157,000 rooms in 35 countries across Asia, Europe and the US under its operation (as of March 2021). Approximately 5,130 employees work for the company worldwide with 3,600 of them based in India.

Since the beginning, OYO’s business has been focused on reshaping the short-stay accommodation space in the country. Its business is typically asset-light and technology-driven meaning that the company doesn’t own any hotels or storefronts listed on its platform. Rather, it benefits from the “Patrons” leasing their spaces to customers via its platform (although lately it has branched out into leasing and franchising its own properties as well, to a certain extent).

Let’s break this down.

- OYO sells hotel and home inventory directly to customers on its own platform or through online travel aggregators (OTAs) like MakeMyTrip, GoIbibo etc.

- It fetches an average revenue share of 20–35% on the gross booking value.

- Plus, the Patrons who list their homes, hotels or resorts on OYO’s platform pay a fixed subscription fee to the site.

This is basically how the company makes money.

This model which enables conversion of fragmented, undervalued, unbranded and under-utilised hospitality assets into branded, digitally-enabled storefronts with a high revenue-generating potential is the characteristic selling point of OYO. During its 10-year stint, the company has managed to provide customers with a diverse selection of medium-to-high-quality hospitality experiences at competitive prices.

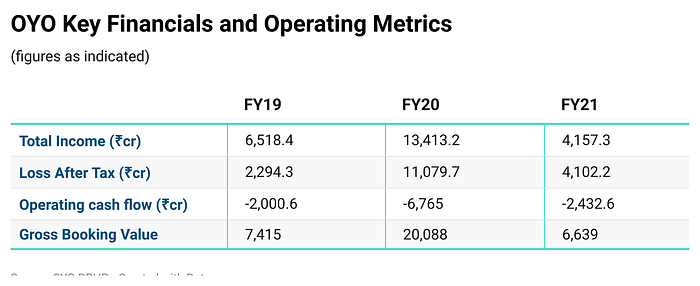

Company Financials

Despite the novel business model and a growing reputation as a “high-flying startup” in India, OYO has had considerable problems generating profits and sustaining growth. The problems intensified in light of several factors — diminishing demand in the hospitality sector due to the pandemic, increasing legal troubles from competitors and a reported wavering of confidence in the bets placed by its largest investor SoftBank, which has been facing its own troubles (the WeWork IPO debacle, Greensill, etc.) for a while now.

In light of the above, OYO announced a series of layoffs in January 2020 and cut down on costs to sustain profitability and growth. It also took a hit in valuation (down from $10bn in 2019 to nearly $9bn now). It is yet to turn a profit.

Most importantly, the company faces a sizable amount of outstanding debt — ₹4,890.56cr ($661.4m). Close to 30% of the proposed issue amount has been earmarked for debt repayment. The company also raised nearly ₹4,920cr ($665.4m) in debt from global institutional investors in July this year as a way to rebuild operations that had been hard hit by the pandemic.

The net cash flow used in operating activities has been consistently negative over the last three fiscals (although the losses are narrowing lately) which indicates difficulty faced by the company in combating operating losses and meeting working capital needs.

This also explains why OYO has stopped offering minimum guarantees to its hospitality partners, meaning that it no longer invests in upgrading the standards of the storefronts it offers on service to customers.

Industry Overview and Investment Risks

In 2019, the total addressable market for short-stay accommodation globally was $1,267bn. Meanwhile, OYO’s serviceable addressable market currently stands at $772bn.

Four markets — India, Indonesia, Malaysia and Europe — account for about 90% of OYO’s overall revenue. Plus, the short-stay accommodation market in these regions is evidently unorganised (India — 92%, South-East Asia — 88%, Europe — largely unorganised).

This is an essential in for platforms like OYO which provide the necessary conduit for online enlistment of these unorganised storefronts and give them a compelling value proposition. Most of these places have limited online presence, revenue management, brand identity and marketing operations.

OYO’s sizable presence in these markets therefore makes it a prime candidate to offer organisational set up to these locations. The company’s recent partnership with Microsoft and consequent plans to offer “smart-room” experiences to customers also signals that technological upgrades in operations is imminent.

But there are quite a few challenges on its path to successfully doing so. First is from third-party distributors (like OTAs, travel management companies etc.) which, although they assist in facilitating the demand for services, don’t extend a helping hand when it comes to back-end management like accounts, revenues etc.

Secondly, more and more organised hospitality players are gaining market share and establishing their independent mandates.

The profit margins are also severely affected when one considers growing financial uncertainties faced by customers, owing to the pandemic and economic downturn. There is a rising demand for value-for-money options (read: very inexpensive) which becomes difficult for aggregators like OYO to cater to without compromising margins.

Apart from these, OYO has its own laundry list of challenges. Hotel partners are increasingly wary of the alleged mismanagement in OYO contracts which also extends as far as breach of trust and cheating in a few instances. Multiple lawsuits (by Zostel, the Competition Commission of India etc.) continue to weigh down the company’s public standing. OYO has also been alleged to favour a “toxic environment” and other troubling incidents which continue to question its reputation.

Having said that, it would be interesting to see how the IPO plays out on Dalal Street on D-Day given the ongoing momentum in valuation for Indian startups. Although some investors are seeking a partial exit, the company still remains popular with fairly encouraging growth prospects.

(Originally published October 6th 2021 in transfin.in)